Professor of Law, and by courtesy, Electrical Engineering at Stanford Law School and Director of Stanford Law School’s Center for Internet and Society.[1]

Introduction

This European Commission consultation is intended to evaluate a proposal to force online services to pay network access fees to broadband companies like Telefonica, Orange and Deutsche Telekom.

These kinds of network fees have never existed in the E.U. and are a violation of the E.U.’s net neutrality law. Mandating such fees would be a radical departure from how the internet has operated and flourished over the last 30 years. Network fees are a threat to the internet in Europe and would set a precedent that could lead to a splintering of the internet across the globe.

Internet service providers (ISPs) have told the European Commission that the rise in traffic is overwhelming and that, without being paid by online companies, they’ll be unable to meet EU connectivity goals and may even go out of business.

Despite claims in studies paid for by the largest telecoms, EU networks are not being overrun with traffic. And while there are issues in some EU member states with deployment of 5G and fiber-to-the-home, telecoms do not lack the funds to build out new infrastructure and don’t need additional money to handle increased traffic.

Traffic is growing at a predictable and steady rate, while the technology to handle more traffic becomes cheaper every year. At the same time, the demand for connectivity continues to grow, with nearly everyone in the E.U. having at least one paid internet connection, most having two (one mobile and one at home), and many having even more (with paid plans for their tablet, automobile, etc.).

For 30 years, the internet has operated by consumers and online services each paying for their own access to the internet. Individuals pay an ISP to connect them to the entire internet, allowing them to use whatever websites and services they choose. Their ISP has the responsibility to connect to other networks to allow them to do so. Online services pay hosting, transit, and content delivery network services (or build and operate undersea cables, data centers, and CDNs themselves) to deliver their traffic to all the other networks on the internet.

This model has led, year over year, to decreasing costs of distribution and ever increasing flows of information. It has allowed everyone – no matter the color of their skin or the size of their wallet – to develop new apps and services or share their ideas with anyone on the Internet at low cost, creating the most powerful communication, educational, and economic engine the world has ever seen.

This proposal asks European legislators to undo that revolution by requiring online services and websites to pay every European ISP, so that each ISP would now be paid twice for the same service it currently provides.

Services that refuse or cannot afford to pay these fees will be either blocked or become extremely slow for EU citizens.

If enacted, the proposal would cause significant harm to small businesses, individual creators, startups, and innovators who will face the choice of paying more to be online, being extremely slow for EU users or being completely unavailable to EU users.

Services that do pay will degrade the quality of their offerings to reduce the tolls they have to pay each ISP. For Europeans, that means no more high-quality YouTube videos; football matches will only be in 4K for the richest customers, and Twitch streams will be downgraded in quality.

This would reverse 30 years of successful internet development that has made the dissemination of information, entertainment, and commerce cheaper every year, and create a global precedent that could lead to the splintering of the internet, as other countries will inevitably follow the E.U.’s lead. In that scenario, every website and service in the world will need to pay, either directly or through their service providers, every ISP in the world, forcing online services to pick-and-choose what portions of the world they serve.

And that’s all without any promise or likelihood that the proposal will increase deployment of 5G and fiber in the E.U.

Taking advantage of political frustrations and grievances with large platforms, ISPs are seeking to have the European Commission turn the internet into a system where ISPs get paid twice for the same service: once, by individuals and companies that pay to get online, and second, by the sites and service providers those individuals or companies seek to use.

Under their proposal, ISPs would not even be required to use this money for increased investment and could simply use it to give bonuses to executives.

This is the first step of ISPs’ plan to eliminate net neutrality. They want to stop being open, utility-like conveyances that allow Europeans to choose to do whatever they want online without interference, and instead become gatekeepers that connect Europeans only with the sites and services that pay the ISPs.

This would be a disaster for the internet not just in Europe, but for the entire world.

The problem does not exist.

The problem with broadband deployment is not lack of funding.

The E.U. has committed to aggressive goals for 100% deployment of both 5G and fiber-to-the-home by 2030. Both of these technologies allow for multi-gig speeds, a huge jump in network bandwidth capacity and reduced latency.

However, the barriers to meeting these goals are often regulatory or simply a business choice not to spend more on infrastructure buildout.

For instance, Spain has seen a huge increase in fiber-to-the-home, with fiber passing over 90% of homes. Telefonica says it will replace all of its copper-based internet connections with fiber by 2025.

Telefonica attributes this success to public policy: “Initial fibre deployment in Spain was started by Telefónica in 2008 when the financial crisis was shaking the Spanish economy but [...] in just six years Spain was at the top of the European ranking. A determinant enabling factor for this: A favourable regulatory framework.”[2]

Spain isn’t alone. Latvia and Portugal are over 90% of homes passed by fiber; Romania, Bulgaria and Sweden are all over 84%; while France, Denmark, Luxembourg and Slovenia each exçeed over 75%.[3]

As these successes show, it’s not a question of capital. Instead, other European countries face issues with complex permitting processes, a lack of digging capacity or a reluctance by ISPs to invest in upgrading their network infrastructure, either as a financial or political decision or both.

In its 2019 and 2021 reports regarding fiber and wireless buildout, the German Monopoly Commission cited many issues: the lack of profitability of deployment projects, a lack of policy mechanism to target government subsidies for infrastructure in unprofitable areas, legal and bureaucratic hurdles, scarce civil engineering capacities, outdated price regulations, and not enough spectrum auctions. It also cited a need to require open access for Deutsche Telekom's fiber.[4]

None of these issues relate to a lack of funding or a crippling amount of traffic.

The consultation appears to suggest there is a funding gap: “Massive investments in network infrastructure are still needed to achieve Europe’s Digital Decade goals. The latest estimates quantify the investment needs until 2030 at around €174bn.”

In a 2021 blog post, Deutsche Telekom suggested that €300bn would be needed to meet the 2030 goal.[5]

But as ETNO, the lobbying group for the E.U.’s largest telecoms, points out current infrastructure investment by EU telecoms is already over €50bn a year: “The European telecom sector has achieved a record CapEx of €52.5bn in 2020, up from €51.7bn in 2019, the highest for four years. This reflects investment efforts in fibre and 5G networks.”[6]

That’s resulted in significant gains: “FTTH coverage in Europe has passed the 50% mark and reached 51.6% of the total next generation access (NGA) connections, [and] the percentage of population covered by 5G in Europe has almost doubled between 2020 and 2021, reaching 62% last year compared to 30% the previous year.”

Non-ETNO member telecoms, as well as tower companies, are also investing in next generation infrastructure.

If ETNO members’ level of investment continues, and there’s no reason to suspect it will not, the current level of investment by 2030 would be over €350bn, more than double what the consultation says is necessary to achieve the 2030 connectivity goals. ETNO’s own State of Digital Communications report from 2022 thus makes clear there’s no lack of funding or progress in infrastructure buildout.

In fact, ETNO’s biggest concern appears to be that users aren’t convinced yet that they need 5G, even when it's available, and that people are not using as much mobile data as telecoms would like them to:

“Uptake of 5G in Europe has been lagging behind: despite being available to 62% of the population, 5G in Europe constitutes only 2.8% of the total mobile connections, compared to 13.4% in the US and 29.3% in South Korea.”

Data usage is also lower in Europe: “[T]he average mobile data usage per capita per month, in 2020, was 8.52 GB in Europe, 10.62 GB in the US and 12.52 GB in South Korea.”

ETNO admitted, “The take-up of 5G smartphones and connectivity was not as quick as initially predicted,” and that “it may be that lower intensity of [mobile] usage [...] makes Europeans less inclined to upgrade.”[7]

Forcing content providers to pay broadband providers will not lead to more network deployment.

The ETNO proposal to force online service providers to pay ISPs directly has no mechanism that requires ISPs to use the additional money to fund infrastructure buildout beyond their current and usual expenditures.

In fact, what we saw in the telephony world is that such payments led to less infrastructure buildout. In the telephony world, countries charge termination fees for long distance calls that originate outside their borders to parties inside their borders. These termination fees led to international calls that cost dollars per minute, because countries, like ISPs today, have a monopoly over reaching the customers in their country or network.

Countries justified the high fees on the grounds that the money would be used to build out infrastructure, but that’s not what happened.

A Mercatus study published in 2012, the last time this kind of proposal was seriously considered, found a negative correlation between high network fees and infrastructure buildout. In other words, the more a nation charged for international long-distance calls, the less new telecommunications infrastructure got built:[8]

“High international telephone collection rates have not led to greater buildout and adoption of telecommunications infrastructure in the past two decades. It seems unlikely, therefore, that adopting a sender-pays model for Internet traffic would increase buildout of Internet infrastructure today.”

Furthermore, as we’ve seen in other contexts, funding is fungible. In the U.S., more than 35 states instituted lottery systems, with many of them dedicating most or all of the proceeds to education. However, that funding turned out to be fungible, and education budgets in lottery states did not rise. A comprehensive study in 2001 found that “lottery revenues earmarked for education are found to have no impact on education expenditures,” and it’s now widely accepted among economists that such funding mechanisms do not increase investments.[9]

It is not even clear that ISPs actually have the capacity to build out more quickly even if they were given a windfall and decided to spend it on infrastructure. As we’ve seen in Germany, the slow pace of next generation telecom rollout is hampered by issues that money doesn’t solve, including bureaucratic hurdles and a lack of spectrum.

The proposal is based on flawed assumptions.

Users, not services, cause traffic.

Netflix doesn’t broadcast videos. YouTube doesn’t randomly send a World Cup match recap to an ISP’s paying customer. Cloudflare doesn’t send a cat GIF from one of its clients to users at random (however fun that might be).

Users choose to watch a Netflix movie, a YouTube clip or a funny GIF on a website. Users choose to upload video, or livestream from their mobile, or make a video call to a family member. Users pay their ISP to deliver traffic upstream and downstream, to and from the sites and services that the user chooses to use. The user creates the traffic over a connection they paid to use.

It is unfortunate then to see the European Commission adopt the language of ISPs by calling online services “Large Traffic Generators” or LTGs. This framing incorrectly blames popular online services for sending traffic to end users.

It’s a perplexing frame, both because it’s inaccurate and oddly resentful. Users only pay ISPs to get online because there are online services they want to use. It’s not quite clear why ISPs resent the services that create the demand for the ISPs’ product; imagine a beach resort being angry that pleasant weather, pretty sunsets, fine sand, and warm water make people rent their rooms.

Some ETNO literature shines some light on the motivation, saying that it’s unfair that platforms like Google and Facebook are more profitable than ISPs are, despite the fact that they are very different kinds of businesses. It’s somewhat akin to electrical utilities throwing a fit that TV manufacturers, popular TV networks, and hit TV shows have higher profits than the electric companies do, and demanding that they pay to build out electrical lines.[10]

Traffic levels are not unsustainable or growing at an unprecedented rate.

Internet traffic has been growing for decades. ISPs, backbone providers, IXPs, CDNs and hosting providers understand this and continually build out new capacity, whether that’s new undersea cables, data centers, additional network ports, and upgraded network protocols.

While there was a one-time upsurge in internet usage due to the pandemic, overall traffic growth has returned to pre-pandemic predictable growth rates, according to multiple independent authorities.

Telegeography reports that: “With the initial rapid traffic growth due to COVID-19 continuing to wane in 2022, many global networks appear to have started to return to more typical rates of utilization. Global average and peak utilization rates were essentially unchanged from the year before [...]”[11]

Sandvine reported a global traffic volume increase of just 23% from 2021 to 2022.[12] Ericsson projects a slowdown in mobile growth as well, projecting an 18% year-over-year growth in mobile data volumes for Europe through 2028.[13]

ISPs like to throw out big numbers claiming that traffic is overwhelming their networks, but often when they do, it points out just the opposite.

In a breathless 2022 blog post, Wolfgang Kopf, a senior VP at Deutsche Telekom, said that YouTube was the largest source of traffic on its mobile network in 2021, and claimed that “unchecked increases in traffic volumes caused and monetized by a few large Internet platforms are not sustainable.”[14]

However, those YouTube traffic figures worked out to 7 Mbs of data per Telekom mobile subscriber per day, or about 30 seconds of a typical YouTube video.[15] It’s a miracle their network doesn’t crash every day under such a load.

It’s also hard to square that concern about unsustainable traffic with ETNO’s own worries we saw earlier that mobile users aren’t using enough data and aren’t adopting more expensive, faster 5G plans.

The telecom industry can’t simultaneously be worried about data overwhelming their mobile networks and be concerned that EU mobile users aren’t using enough data.

Increased traffic does not result in higher costs.

Networking equipment works just as consumer electronics and services such as computers, cellphones, and online services do: they get faster, cheaper and more powerful every year.

So the costs of deploying and operating broadband infrastructure drop every year. Routers become cheaper, transit becomes cheaper, and the next generation of networking like 5G and fiber are capable of 1000x more capacity than the equipment they replace.[16] And ISPs are moving away from having network hardware control network operations, much as people are moving from desktop word processors to using Google Docs or Microsoft 365. This process, called network virtualization, makes it much faster, easier, and cheaper to modify software, control the network, and configure new capacity.

In 2016, AT&T’s CFO said that the company’s move to network virtualization let AT&T add 2.5 times more capacity at 75% of the capital cost than previously.[17]

While ISPs share scary numbers about the cost of additional traffic in studies intended to sway public policy, they tell a different story to their investors to whom they cannot lie.

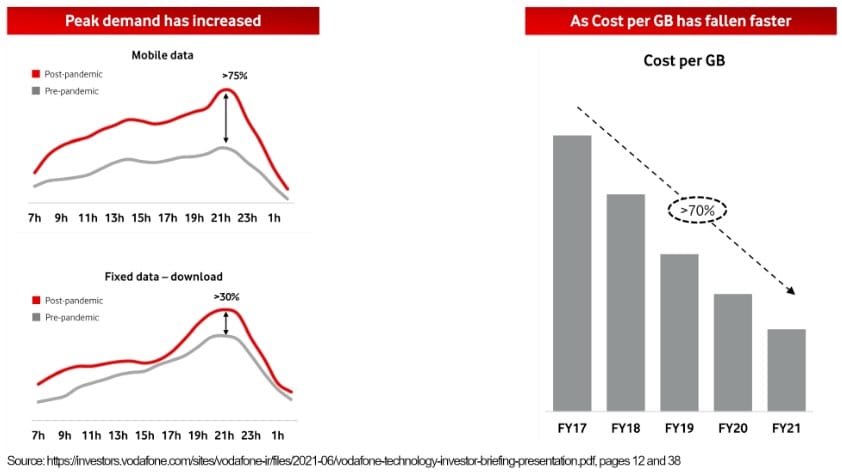

For example, a 2021 Vodafone investor presentation showed that while traffic had risen significantly from 2017 to 2021, the cost of moving that data had fallen even faster: “Peak demand has increased as the cost per GB has fallen faster.”[18]

Notably those numbers pre-date Vodafone’s rollout of 5G that has up to 1000x the capacity of 4G and the ability to handle many more devices, all while using less energy.

A 2022 Analysys Mason study found that “Network-related costs for ISPs have remained stable over time even while traffic volumes have grown significantly. Data traffic only drives a small share of ISP costs.”[19]

The study found that, from 2018 to 2021, “network-related ISP costs increased by 3% in total over three years, whilst network traffic increased by over 160%.”

Notably just prior to the submission deadline for this consultation, Deutsche Telekom, which is claiming that data growth is unsustainable and that it can’t keep going without mandated payments from online services, reported its 2023 Q1 financial results. It upped its guidance because its broadband business is doing so well, with increased revenues in mobile putting it on track to make a €40bn profit in 2023, with free cash flow of €16bn.[20]

Online services spend billions of dollars optimizing traffic, despite ISP’s claims to the contrary.

ISPs like to claim that online services have no incentive to optimize their traffic delivery unless ISPs tax them.

Here’s Telefonica, for instance: “Additionally, absent any direct traffic cost on telecom networks, there is no price incentive for OTTs to generate traffic more efficiently and thus insufficient motivations to control and reduce traffic related energy consumption and CO₂ emissions to limit the carbon footprint...”[21] (emphasis added)

This is an absurd claim. Large infrastructure providers and platforms spend billions in R&D to make their data centers as efficient as possible, even going so far to design their own chips and hardware. And since they pay their own data transport costs and electricity bills, they have every incentive to make their traffic as efficient as possible.

Even beyond that, every online application and website works to make their site as lean and fast as possible. Just as one example, every serious online company, website and blogger uses a CDN to host their traffic locally around the world. No application or service needs to pay an ISP to have an incentive to optimize their site; slow performance dooms a site to irrelevance. A fast data-optimized app is table stakes in the ultra-competitive online market.

Content providers already contribute by investing in content, applications, services, and infrastructure.

Without content providers, there would be no market for internet access. Netflix, Google, and the millions of other sites and services on the internet are the very reason that any ISP’s customers purchase access to the internet.

And when new content and services that require more data come to market, customers are motivated to upgrade to faster, enhanced, and more expensive internet plans. Innovation by content providers directly leads to increased revenue and profits for ISPs, which is just one way that content providers contribute to making this market work.

Content providers take huge risks that ISPs never have to bear. ISPs operate in a stable, low-risk market with limited competition where demand for their product is created by others. In contrast, content providers, startups and venture capitalists take significant risks in developing costly new content and applications that may or may not take off. The five largest tech companies spent nearly US $400bn on R&D and capital investments in 2022 alone.[22] And most new applications fail. But ISPs benefit from the successes of that speculative development and VC investment, while facing none of the downside risk.

On the network infrastructure front, content providers spend billions of dollars every year to bring data right to the ISPs’ doorsteps. The largest content providers build and operate expensive, large data centers to host their data, while nearly every other player rents similar facilities via cloud services and CDNs. Then, the large platforms, cloud services and CDNs transport that data across the world by constructing or leasing undersea and terrestrial cables. Once they get that data across continents, they interconnect directly with networks of all sizes and store copies of their data close to customers to speed up downloads.

All of these investments make it easier and faster for ISPs to get online services and website data to their customers as the last step in a long chain of data transportation. Which is to say not only do online companies pay to create movies and create new applications, they spend billions to bring all of that to the doorsteps of ISPs around the world (and even sometimes cache the data inside ISPs’ networks), which drastically cuts the ISPs’ own transit connection costs.

That’s not cheap to do. These investments totaled US $883bn worldwide over the last decade–including over US $201bn spent in Europe. Because content providers pay to bring data 99% of the way to customers, European ISPs only need to worry about getting that data across the last mile, saving them €950mn in 2022.[23]

Contrary to ETNO’s complaints, content providers clearly “contribute[...] in a fair and proportionate manner” to making the internet work.

As Europe’s top telecom regulator, BEREC, made clear in its September report on the network fee proposal: “There is no evidence that operators’ network costs are not fully covered and paid for in the internet value chain. […] There is no evidence of “free-riding.”[24]

Accurate traffic attribution is impossible.

Network fee proposals must rely on accurately identifying and measuring sources of traffic, which is challenging, if not impossible to do.

Most traffic is encrypted and increasingly uses modern protocols (QUIC/HTTPS3) that prevent network surveillance. For example, Sandvine lists “Generic QUIC” and “Generic HTTP Media Stream”–different types of encrypted, unidentified video traffic–as the top 3 and top 4 video apps globally, with overall shares of total traffic of 5.41% and 4.33%, respectively.[25]

If a content provider interconnects directly with an internet access provider or operates its own CDN, it is easier to attribute the traffic to that service.

However, if a content provider’s data comes into the network through another network provider or a third-party CDN, its data traffic is mixed in with other applications, making it much harder and often impossible to attribute.

Additionally, users increasingly use privacy and security tools such VPNs and Apple’s Private Relay that completely hide their traffic from network snooping, including attribution tools.[26]

All that means that traffic attribution will never be accurate, so disputes will be common and difficult to resolve. Companies subject to the fees might take steps that make it harder to identify their traffic, e.g., by no longer directly interconnecting with internet access providers or moving some of their offerings to third-party CDNs.

Finally, apps become popular and fall out of favor quickly on the internet, so traffic shares change continuously, making measurement and negotiation a costly, ongoing challenge. For example, from 2021 to 2022, Facebook’s share of global traffic dropped from 15.1% to 6.5%, while Microsoft’s share grew from 3.3% to 5.1%.[27] Thus, a company might meet the network fee threshold during one month, but not the next.

The proposal violates net neutrality.

Prohibiting ISPs from charging websites for delivering the traffic the ISPs’ customers requested is a key net neutrality protection.

In the U.S., the 2010 and 2015 Open Internet Orders explicitly prohibited these fees, and the 2015 Order made clear that ISPs cannot circumvent Open Internet protections at interconnection points where data enters their network.[28] California’s net neutrality law includes the same protections.[29]

Europe’s largest telecoms and the Commission claim that network fees won’t violate net neutrality, but that’s not possible.

Network fees violate the Open Internet Regulation.

Charging network fees violates both Art. 3(3) and Art. 3(1) of the Open internet Regulation.

Art. 3(3), subparagraph 1 of the Open Internet Regulation prohibits ISPs from discriminating among applications, content, and services. In 2020 and 2021, the European Court of Justice held that this rule prohibits ISPs from treating applications differently either technically or economically. The rule prohibits ISPs from slowing down Netflix, while putting their own online video service in a fast lane. That would be technical discrimination.

It also prohibits ISPs from charging a different price for the data used by WhatsApp than for the data used by an ISP’s own messaging app. That would be economic discrimination. Charging selected content providers for the data traffic associated with their content treats content providers that have to pay differently from those that are exempted. This kind of economic discrimination directly violates Art. 3(3), subparagraph 1.

Additionally, Art. 3(1) of the Open Internet Regulation protects Europeans’ right to use their internet service to access the applications of their choice. The rule protects Europeans’ ability to access all of the content available on the Internet, not just the apps and sites that have paid their ISPs. Apps and sites that do not pay the required fee would not be accessible to an ISP’s subscribers, preventing its subscribers from accessing the content, applications, and services of their choice. This violates Art. 3(1).

Network fees violate the Open Internet Regulation. Network fees violate Art. 3(3), subparagraph 1 and Art. 3(1) of the Open Internet Regulation. Art. 3(3), subparagraph 1 requires providers of internet access services[30] to “treat all traffic equally, when providing internet access services, without discrimination, restriction or interference, and irrespective of the sender and receiver, the content accessed or distributed, the applications or services used or provided.” According to the European Court of Justice’s 2020 and 2021 zero-rating decisions, Art. 3(3), subparagraph 1 is a general non-discrimination rule that applies equally to technical discrimination (e.g. blocking or slowing down traffic) and economic discrimination (e.g., not counting traffic associated with certain applications against customers’ data caps).[31] The Court found that internet access providers violate Art. 3(3), subparagraph 1 when they offer so-called “zero-rating” plans that exempt select applications from their customers’ monthly data caps. According to the Court, such plans make a distinction among traffic by not counting the traffic associated with some applications–the “zero-rated” apps–towards their customers’ data caps, which violates Art. 3(3), subparagraph 1. When charging the network fees, internet access providers charge some content providers for the traffic associated with their content, but not others. Thus, just like discriminatory zero-rating plans, network fees make a distinction among traffic based on the sender, content, application, or service, which violates Art. 3(3), subparagraph 1.[32] Network fees are not justified under Art. 3(3), subparagraph 2 or 3 – the only exceptions to Art. 3(3), subparagraph 1 that the Open Internet Regulation recognizes.[33] Network fees do not serve a traffic management purpose and are not tied to “objectively different technical quality of service requirements of specific categories of traffic.” Thus, they do not constitute reasonable traffic management under Art. 3(3), subparagraph 2. They do not meet any of the other exceptions in Art. 3(3), subparagraph 3, either. Network fees also violate end users’ rights to access the content, applications, and services of their choice under Art. 3(1). Applications subject to the fee are not accessible to European internet users unless the application provider pays the fee, making it impossible for European internet users to exercise their right to use the applications of their choice. Network fees violate the Open Internet Regulation regardless of whether they are included in interconnection agreements. It is unclear whether providers of internet access service would charge content providers directly or whether network fees would be included in interconnection agreements. While large ISPs like the ETNO members often interconnect directly with larger content providers, many internet access providers do not directly interconnect with content providers. Thus, these providers would have to charge network fees directly, which would violate the Regulation. In any event, network fees would violate the Open Internet Regulation even if they were included in interconnection agreements. That’s because charging such fees as part of interconnection agreements either directly violates the Regulation or circumvents the Regulation, which is also prohibited. The Open Internet Regulation does not mention interconnection, but it applies to the provision of internet access service. Thus, the Regulation directly applies to an internet access provider’s interconnection practices if connecting internet access customers to the rest of the internet is part of the provision of internet access service. The Open Internet Regulation is silent on this question. Europeans buy internet access services to get access to the entire internet, not just to their ISP’s network. Consistent with that, the Regulation defines internet access service as a service that “provides access to the internet, and thereby connectivity to virtually all end points of the internet.”[34] The Regulation explicitly protects end users’ right to access and use the applications of their choice, “regardless of the location, origin or destination of the information, content, application or service.”[35] This suggests that interconnecting with other providers so an internet access provider’s customers can access all endpoints on the internet is an integral part of the provision of internet access service and, therefore, directly subject to the Regulation. In this case, network fees would directly violate Art. 3(3), subparagraph 1 and Art. 3(1), regardless of whether they are included in an interconnection agreement or charged separately. Even if the Open Internet Regulation does not apply directly to an internet access provider’s interconnection practices, including network fees in interconnection agreements would still violate the Regulation. According to Recital 7 of the Regulation, commercial practices of providers of internet access services should not circumvent the provisions of the Open Internet Regulation. As BEREC’s Net Neutrality Guidelines recognize, this prohibits ISPs from circumventing the provisions of the Open Internet Regulation via interconnection.[36] The Open Internet Regulation prevents ISPs from blocking apps inside their network. Just as ISPs cannot circumvent that ban by blocking apps from entering their network at the point of interconnection, ISPs cannot circumvent the ban on network fees by including them in an interconnection agreement. |

Selective network fees harm everyone.

Selective network fees violate net neutrality principles by distorting competition between streaming video, music, cloud, gaming services, as well as hosting services and CDNs.

Selective network fees present serious competition problems. By charging only some companies and not their competitors, selective network fees would operate as a “tax” on the most popular businesses in a wide range of markets. This would distort competition in many markets that are currently highly competitive. Netflix would be forced to pay, while Disney+, TRT İzle, myCanel, and Tubi can compete at a much lower cost. No matter which video service users prefer, those exempted from the tax will have a competitive advantage solely because of their lower costs.

This makes no sense. Packets are packets: streaming video from a less popular provider burdens the network just as much as video from a popular service, and the users of both services have already compensated their ISP for that burden. Net neutrality means that users decide which applications succeed, without interference from their ISPs. By charging network fees and making it harder for affected applications to compete, ISPs violate that principle.

This problem is even worse because ISPs compete in many of these markets themselves. ISP-owned online services like Telefonica’s Movistar Música, Deutsche Telekom's MagentaTV, and Orange Cloud will all gain a huge advantage over competitors paying fees. In fact, they’ll even get an extra boost because their parent company will be on the receiving end of these payments.

In essence, popular services like Netflix would be forced to pay fees directly to their competitor. The result will be a three-tier system with the most popular players paying the tax, ISP-owned content and apps getting a bonus, and small and medium providers left in the middle: they aren’t forced to pay but are still disadvantaged.

The only way to avoid the competitive distortion from network fees is to charge all content providers an equal tax on every bit and byte. But that would violate net neutrality, too,[37] and would fundamentally change how the internet operates. Some sites and services will not pay every ISP in the E.U., either by choice or financial necessity. Internet access as we know it would disappear.

Instead, we’d be in the world of cable: Our online choices would be limited to the services that paid a particular ISP the fees that ISP demands, the very situation net neutrality was intended to prevent. While Telefonica has made it clear that’s what they’d like the future of connectivity to be, that’s not the internet anyone other than an ISP executive wants.[38]

Network fees will harm European consumers.

Because popular content providers will be facing significantly higher costs, many of the services that Europeans like to use will become more expensive, whether that’s gaming, video streaming, or online backups. ISPs can charge exorbitant network fees because they have what is called a termination monopoly. Because the only way that content gets to an ISP’s subscribers is through the ISP’s pipes, large ISPs have all the bargaining power and can force content providers to pay up or go under. These monopoly fees end up getting passed on to users in the form of higher prices.

We’ve seen this before in the U.S.. For example, when Comcast forced Netflix into paying for access to Comcast’s internet service customers, Netflix had to raise its prices.[39] There is no reason to expect it to play out differently for European consumers this time around.

As an alternative to raising prices, affected apps and services may restructure their EU offerings to lower network fees. This isn’t hypothetical. We’ve seen this exact behavior happen in South Korea in response to a similar attempt to charge network fees.

Because the fees are tied to bandwidth, the easiest option for platforms is to limit or end high bandwidth services. That’s why Amazon’s Twitch, a popular livestreaming service, eliminated high definition live video streams in South Korea and later removed the ability of South Koreans to watch recorded live streams at all. Like South Koreans, European users will no longer have the choice to access high quality content online; their ISP will have eliminated that choice by adopting these fees and making it too expensive for content providers to offer these services.

Efforts to cut bandwidth could spell the end of free services as well. While Twitch only had to reduce the quality of its content, other providers might not be able to survive. It’s hard to see how the business model of any free or ad-supported high bandwidth service continues to work when the costs of providing that service skyrocket. Free photo and email storage limits will drop. Popular video streaming platforms and services like YouTube or Tubi may need to eliminate free ad-supported video in Europe, while keeping higher quality streams for paying European customers and customers abroad.

Another tool to reduce or avoid these fees would be to simply move content out of Europe. All of the investments that content providers make in bringing data across the world stop making economic sense when they are charged extra for bringing that data right to the ISP’s door. Hosting that data in the U.K. or somewhere else abroad, if structured correctly, could reduce what content providers need to pay for data transport and help them avoid paying network fees by making their service harder to identify. But because content located further away loads more slowly, it will also reduce the quality they can offer, again harming user choice and further degrading the European internet.

Adopting the network fee proposal will put us in a world where Americans can stream crystal-clear Champions League matches and highlights, while Europeans are forced to watch low-quality streams or pay high prices just to watch the match at all. There is no reason to inflict that severe harm on European consumers by adopting this proposal.

Network fees will harm European businesses, creators, and nonprofits.

While ETNO and this proceeding pitch these selective network fees as a targeted solution that will only harm large American tech companies, that’s simply not how the modern internet works. Almost all EU organizations, large and small, as well as individual creators, use services provided by these companies. These include cloud hosting services and CDNs like Amazon Web Services and Google Cloud, productivity services like Google Docs and Microsoft Teams, and social media platforms like Instagram.

Even if only the large platforms will be forced to pay network fees directly, European businesses will have to pay higher prices for the platform’s services or switch to low quality alternatives for the services they need to function.

Take for example, ARD, the Association of Public Broadcasting Corporations in the Federal Republic of Germany, composed of nine regional broadcasters and the international state-funded broadcaster Deutsche Welle. ARD has 100 million views a year using Google Cloud services, and would likely either have to pay higher prices to accommodate network fees or undertake a costly process of moving to a lower quality alternative host that does not have to pay network fees.[40] Faced with higher prices for common cloud-based services, others might not transition to the cloud in the first place. These fees thus will put Europe even further behind on cloud adoption and work directly against the Commission's stated goal of increasing migration to the cloud.

Reaching Europeans with advertising will become more expensive. The platforms will have no choice but to raise the price per ad for content in Europe, meaning European advertisers will be paying more for less.

European businesses, organizations, and content creators will also suffer from reductions in the quality of service they receive and can offer to European customers. Any organization that distributes video content through YouTube and other large platforms would likely have the resolution of their videos degraded in the E.U. or have their ad revenue slashed. Individual content creators on YouTube, Instagram, Twitch, and other platforms will find it harder to make a living because platforms will have to keep a larger share of ad revenue to pay ISPs. Network fees will reduce budgets for creating new movies, paying creators, and improving services. And if the large platforms move their services out of the E.U., webpages and services offered by European businesses that rely on the platform’s services will load more slowly and will have to use less bandwidth to remain usable.

All of these impacts are particularly problematic for small businesses, startups, and nonprofits. In South Korea, for example, Cloudflare reduced the quality of service they offer under their free tier. As part of its service, Cloudflare stores its customers’ content in locations worldwide so it loads faster for people everywhere. Their free tier allows many startups, small businesses, and nonprofit sites and services to operate quickly and safely around the world–even if they normally couldn’t afford to pay for such a service. But because of the new fees, Cloudflare couldn’t afford to continue operating their free tier the same way in South Korea. Instead, only paying Cloudflare customers can have their videos, files, and photos stored in South Korea, while those on the free tier are hosted abroad. This means that smaller players load much more slowly–if at all–for Korean users, hurting both Koreans and the ability of Cloudflare’s free-level customers to break into the South Korean market.

Thus, network fees would directly harm and indirectly tax tens of thousands of EU businesses, creators, and nonprofits, transferring money from them to giant, incumbent telecommunications companies without even a promise that new infrastructure would be built.

Network fees distort competition among ISPs.

Allowing these fees will also distort competition in the market for internet services. Large ISPs will get more money from network fees than smaller ones, simply because they have more subscribers. Large ISPs will get this large influx of money, regardless of whether they (or the country) already reached their deployment goals or whether other companies are more efficient in deploying new infrastructure. This disadvantages challengers and new entrants.

Compounding the problem, larger ISPs can demand a larger fee per subscriber, as we saw in the U.S.[41] Small ISPs lack the bargaining power or personnel to negotiate with large platforms. This will favor consolidation and reduce ISP competition, resulting in higher prices and worse service for European users.

Network fees would undo decades of successful Internet economics.

Requiring content providers to pay ISPs fees that have never existed before would be a disastrous return to the economic model for telephony where telecom companies leveraged their termination monopolies to make long-distance telephone service prohibitively expensive.

Since every phone company and country has a monopoly over their customers they were able to, and still do, charge exorbitant termination fees to everyone wanting to call their customers from outside their network or country.

This is what led to prices as high as USD $4-5 per minute for international calls. Governments that realized this was a problem created a regulatory monster trying to rein in these termination fees, which remain unconnected to the actual cost even to this day. Ironically, the invention that finally crushed this price-gouging scheme was the internet, where the rise of VoIP and services like Skype and Facetime let people connect with loved ones and business partners around the world for pennies, and eventually for free.

Broadband providers have the same monopoly over their internet service customers that telecom providers had in the heyday of traditional voice telephony. That means it’s inevitable that if they are granted their wish that online services must pay them in order to reach their customers, the price gouging will return.

We saw this happen in the U.S. in 2013-15, when the largest ISPs in the country demanded outrageous payments from large online services and backbone providers, and throttled the doors to their network for those who did not pay. Tens of millions of Americans suffered from web sites that didn’t load, games that wouldn’t play, and videos that stuttered.[42] The throttling did not stop, despite citizens howling and loads of bad press, until sites paid the monopoly-level fees. This behavior continued for years until the FCC put a stop to it in 2015.

The internet has thrived and grown remarkably in 30 years, thanks to an economic model where users pay their ISP to be able to choose what they want to do on the internet, without interference from the companies they pay to get online. In three decades, the internet grew from being a playground for geeks to the most powerful, flexible and world-changing communication platform the world has ever seen, and an indispensable tool to every facet of our lives and economy.

And while the internet is far from perfect, the solution to its growing pains is not going to be found in overturning its fundamental economics and tossing out net neutrality in a fruitless attempt to solve a non-existent problem.

Barbara van Schewick is one of the world’s leading experts on net neutrality, a professor at Stanford Law School, and the director of Stanford Law School’s Center for Internet and Society.

Download comments as a PDF.

Read comments online in a Google doc.

[1] I have not been retained or paid by anyone to participate in this proceeding. Additional information on my funding is available here: http://cyberlaw.stanford.edu/about/people/barbara-van-schewick.

[2] Telefónica, "A Digital Deal to Build Back Better," June 2021, p. 35; Telefónica, "Why Spain is a Case Study for Super-Fast Broadband".

[3] TelcoTitans, "FTTH Conference: Fibre-Rich Spain Faces Final Rural Connectivity Hurdle".

[4] Monopolkommission, "12th Sector Report Telecommunications 2021"; Monopolkommission, "11th Sector Report Telecommunications" .

[5] ETNO, "The State of Digital Communications 2022" .

[6] Ibid.

[7] Ibid. p. 43.

[8] Ars Technica, "Sender-Pays Rule Doesn't Necessarily Increase Telecom Investment" and Eli Dourado, "Do High International Telecom Rates Buy Telecom Sector Growth? An Empirical Investigation of the Sender-Pays Rule" (Mercatus Center and Department of Economics at George Mason University, November 2012).

[9] Thomas A. Garrett, "Earmarked Lottery Revenues for Education: A New Test of Fungibility," Journal of Education Finance 26, no. 3 (Winter 2001): 219-238.

[10] Notably, thousands of other businesses that rely on the internet and use the services that ISPs want to tax would envy the ceaseless demand ISPs have for their services and the blue chip telecoms’ substantial margins and market caps.

[11] TeleGeography, "2023 State of the Network Report".

[12] Sandvine, "2023 Global Internet Phenomena" p. 9 .

[13] Ericsson, "Ericsson Mobility Report" November 2022, p. 25.

[14] “YouTube generates the most data traffic on Telekom's mobile network: In 2021, it averaged 357 terabytes per day, an increase of a remarkable 96% over the previous year.” Deutsche Telekom, "How Sustainable is Unlimited Data Growth on the Internet?".

DT had 50M mobile subscribers as of June 2021. Deutsche Telekom, "Interim Report Q2 2021: Development of Business in the Operating Segments - Germany".

[15] van der Berg, “Internet Traffic Growth Is Not Out of Control, and Nothing Like Telcos Want You To Believe”.

[16] Cisco, "5G vs. 4G: What's the Difference?".

[17] FierceWireless, "T-Mobile, AT&T, and Verizon Maintain Capex Spending Despite Incentive Auction".

[18] Vodafone Technology, “Investor Briefing Presentation”, June 2021.

[19] Analysys Mason, "The Impact of Tech Companies' Network Investment on the Economics of Broadband ISPs".

[20] Results. “In its home market, Deutsche Telekom is enjoying rapid customer growth in all areas. [...] The number of customers using an FTTH line increased by 37% year-on-year to 769,000. With 274,000 new branded customers, Telekom Deutschland also had an exceptionally successful start to the new year in mobile communications [...] [M]obile service revenues increased by 1.7% compared with the prior-year period. Revenue in the Germany operating segment increased by 2.3% year-on-year on an organic basis in the first three months of the year to €6.1bn. Broadband revenues were a key driver here. At the same time, adjusted EBITDA AL increased by 3.1%.”

[21] Telefónica, "The Unsurmountable Cost of OTTs' Traffic for Europe".

[22] CAP Investment Data: The Economist, "Mastering the Machine: Big Tech and the Pursuit of AI Dominance".

[23] Analysys Mason, "The Impact of Tech Companies' Network Investment on the Economics of Broadband ISPs".

[24] BEREC, "BEREC Preliminary Assessment of the Underlying Assumptions of Payments from Large CAPs to ISPs".

[25] Sandvine, "2023 Global Internet Phenomena" p. 15.

[26] Ibid. p. 25. “The challenge for operators is that QUIC obfuscate[s] what’s happening on networks. That’s true overall with the rise in encryption (i.e., Apple iCloud Private Relay), QUIC, and HTTP/3 traffic, all of which leads to a flood of “unknown” or “other” traffic…”.

[27] Ibid. p. 10.

[28] The 2010 Order defined network fees as a kind of blocking, while the 2015 Order defined them both as a kind of blocking and a kind of degradation. FCC 2010 Open Internet Order, paras. 24, 67; FCC 2015 Open Internet Order, paras. 113, 120, 206.

[29] SB 822, §3101(a)(3),(9)&(b).

[30] I use “provider of internet access service,” “internet service provider,” and “ISP” interchangeably.

[31] ECJ 2020 Telenor Decision; ECJ 2021 Vodafone Tethering Decision; ECJ 2021 Vodafone Roaming Decision; ECJ 2021 Telekom Decision. For a discussion, see van Schewick, Barbara (2022), The Impact of the ECJ’s 2020 and 2021 Zero-rating Judgments on Zero-rating and Differentiated Pricing in the European Union. White Paper Submitted to the Public Consultation on the Draft BEREC Guidelines on the Implementation of the Open Internet Regulation, p. 12 and Part 3, Section 1.

[32] Network fees make a distinction among traffic by charging some content providers for the traffic associated with their content, but not others. That is same kind of distinction that, according to the European Court of Justice, invalidated zero-rating plans: “A ‘zero tariff’ option, such as that at issue in the main proceedings, draws a distinction within internet traffic, on the basis of commercial considerations, by not counting towards the basic package traffic to partner applications. Consequently, such a commercial practice does not satisfy the general obligation of equal treatment of traffic, without discrimination or interference, laid down in the first subparagraph of Article 3(3) of Regulation 2015/2120.” (2021 Vodafone Tethering Decision, para. 28).

[33] 2020 Telenor decision, paras. 48-50; 2021 Vodafone Roaming decision, paras. 25, 27.

[34] Art. 2(2): “‘[I]nternet access service’ means a publicly available electronic communications service that provides access to the internet, and thereby connectivity to virtually all end points of the internet, irrespective of the network technology and terminal equipment used.”

[35] Art. 3(1).

[36] BEREC 2022 Net Neutrality Guidelines, para. 6.

[37] See the discussion in the previous section.

[38] Telefónica, "Who Chooses the Number of Sides of a Market?".

[39] Ars Technica, "Netflix comes through with price hike after struggles with Comcast, Verizon".

[40] Google Cloud, "ARD: Building a Digital-First Public Broadcasting Service with Google Cloud".

[41] This happened in the U.S. FCC 2016 Charter/TWC Order, para. 99.

[42] Susan Crawford, "The Cliff and the Slope," Wired.